|

1.0

Traffic Accident - What To Do Next?

- Be calm and do not panic.

- If there are injuries to any persons, call 999 for assistance.

- If there are no injuries, move your vehicle to a safe area

away from traffic, where possible.

- Note the names and addresses of the other driver(s) involved.

- Note the model and vehicle registration number of

the vehicle(s) involved.

- Note names and addresses of witnesses, if any.

- Sketch a simple diagram of the accident scene and

the position of each vehicle right before and after the

accident (Photos of the accident scene, if available,

can be very helpful).

- Exchange information on the names of your respective

insurance companies/takaful operators.

- Do not discuss on whose fault it was. This may complicate

the handling of your claims.

- If your vehicle needs to be towed, ensure that the vehicle

will be sent to the correct workshop. Call your insurance

company/takaful operator or its accident hotline number

for the appropriate workshop.

- Report the accident to the police promptly.

- Inform your insurance company/takaful operator promptly

even if you do not intend to make a claim. The third party

involved in the accident may make a claim against your

insurance company/takaful operator which would cause

you to lose your NCD.

- Complete the claims form in full and include any

additional relevant information. If in doubt, ask your insurance company/takaful operator for advice.

. back

to top

2.0 How To Prevent Your Vehicle From Being Stolen?

2.1 Secure your Vehicle

- Lock your Vehicle .

- Never Leave the vehicle key inside the vehicle unattended.

- Never leave your vehicle's engine running, even if you will

only be away for a minute. Vehicles are commonly stolen at

convenience stores, petrol stations, ATMs and outside house

compounds when owners leave the vehicle engine running

to run errands or to unlock house gates.

- Ensure your vehicle windows are properly closed up.

- Do not leave valuables in your vehicle. However, if you have

to, place valuables out of sight in the boot. Ensure that no

one sees you placing valuables in the boot.

back

to top

2.2 Parking

- Park in well-lit areas - vehicle theft usually occur at night

under the cover of darkness.

- Park in attended lots - vehicle thieves do not like witnesses

and prefer unattended parking lots.

- Park your vehicle in the compound of your house rather

than outside. Lock both your vehicle and the gate for

improved security.

back

to top

2.3 Security

- Professional thieves are able to steal any vehicle.' However,

you can make it difficult for them to steal your vericle.

The more layers of protection on your vehicle, the more

difficult it is to steal.

- Your budget and personal preferences should determine

how many layers of protection and which anti-theft

devices are best for you.

-

Generally available anti-theft devices are:

- Engine immobilizers

- Better door and ignition locks.

- Security patterned or coded keys

- Radio/CD players with security code or removable

face plates

- Window etching

- Car alarm

- Steering wheel/gear/brake pedal locks

- Tracking devices

back

to top

3.0 Private Car - Coverage for each type of cover.

| Types

Cover |

Third party Cover |

Third party, fire

& theft cover |

Comprehensive

Cover |

Liabilities to third

party for:

. injury

. death

. property

loss/damage |

|

|

|

Loss/damage

to own vehicle

due to accidental

fire/theft

|

|

|

|

Loss/damage

to own vehicle due to accident

|

|

|

|

Liabilities to

driver &

passengers

of own vehicle

(property, bodily

injury, death)

|

|

|

|

Exclusions

Your standard motor insurance policy DOES NOT cover:

- Your own death or bodily injury;

- Your liability against claims from your passengers;

- Theft of non-factory fitted vehicle accessories (car stereos,

leather seats, sports rim, etc.) unless otherwise declared.

- Consequential loss, depreciation, wear and tear,

mechanical or electrical breakdown failures or

breakages; and

- Loss/damage arising from an act of nature e.g.

flood, landslide.

However, you may pay additional premiums to cover some of

the above exclusions e.g. flood or your liability against claims

from your passengers. Windscreen and vehicle accessories

covers are also useful extensions to consider for preserving

your No-Claim-Discount (NCD) in the event of a loss/damage.

Please check for other exclusions and extension covers available with your insurance company/agent.

back

to top 4.0

What should you know when buying motor insurance cover

4.1 Insurable interest

Make sure that you buy cover as soon as you purchase a vehicle.

If you buy a used car, you should protect your interest by

purchasing a motor insurance cover as the cover of the previous

owner is no longer valid even if legal ownership transfer has not

been effected with Jabatan Pengangkutan Jalan (JPJ).

back

to top

4.2 Insured Value / Sum Insured

Ensure your vehicle is adequately insured.

New vehicle: sum insured = purchase price.

Others: sum insured = market value of vehicle when policy

is bought.

Under-insurance: if sum insured is less than the market value, you are deemed as self-insuring the difference. In the event

of a loss, you will only be partially compensated.

Over-insurance: if sum insured is higher than market value, maximum compensation is the market value of the vehicle.

You cannot profit from a claim (principle of indemnity).

Determination of market value of your vehicle

is important to avoid under- or over-insurance.

back

to top

4.3 Average Clause

It is applied when you suffer damage to your vehicle which

is under-insured. Your claim will be reduced proportionately

by the uninsured portion, e.g. if you have insured your vehicle

up to 70% of the market value, the insurance company will

only pay 70% of the total repair cost.

back

to top

4.4 Disclosure

Disclose all material facts, e.g. any previous accidents

and modification to engines. If you fail to do so, your

insurance company may refuse your claim or any claim

made by a third party against you. In such cases, you

are personally liable for those claims.

back

to top

4.5 No-Claim-Discount

The premium payable may be reduced by your NCD

entitlement. NCD is 'awarded' if no claim was made

against your policy during the preceding 12 months

of policy. Your NCD entitlement will depend on the

class of your vehicle and number of years of continuous

driving experience without any claim made against

your insurance policy. You will lose your entire NCD

entitlement once an own damage or a third party

claim is made against your policy.

back

to top

4.6 Excess

It is the amount of loss you have to bear while your insurance

company will pay for the balance of your vehicle damage

claim. If you have an 'excess' on your policy, you must pay

the amount of the 'excess' direct to the repairer.

back

to top

4.7 Payment of Premium

- Premium must be made to the agent representing your

insurance company or to your insurance company directly

before cover can be granted.

- Payment can be made by cash, credit card or cheques

(cheques should be made payable only in the name of

the insurance company).

- Insist on a receipt for the premium paid to your insurance

agent or insurance company.

- With the full implementation of the JPJ elNSURANS

system with effect from 2 January 2005, physical cover

notes are no longer issued. However, a statement

containing details of your motor cover will be issued to

you as confirmation of purchase of motor insurance.

- Through the JPJ eINSURANS, all information on insurance

coverage will be channelled electronically by your agent!

insurance company to JPJ.

- Contact the insurance company if you have not received

the insurance policy after one month of purchase.

back

to top

5.0 What you should know when making a claim?

If your car is involved in an accident:

- Take note of the names and addresses of all drivers

involved, make/model and registration numbers of

each vehicle, the drivers' licence numbers, the insurance

particulars and names and addresses of witnesses.

- Make a police report within 24 hours and immediately

notify your insurance company in writing with full

details.

- If your vehicle is damaged, you may either make an own

damage claim or a third party claim:

Own damage claim - making a claim against your own comprehensive policy. However, you will lose your NCD entitlement.

Third party claim - if you are not at fault in the accident, you can submit the claim either directly

to the insurance company of the party at fault,

or if you have a comprehensive policy, to your

insurance company, without losing your NCD

entitlement. You are encouraged to submit

your claim to your own insurance company

for speedier claims processing.

- For own damage claims, call your insurance company

immediately for advice. If your insurance company

recommends or requires that repairs be done at a panel/

authorised workshop, then take your vehicle there as

advised. Your insurance company will reject your claim

if your vehicle is sent to a workshop that is not authorised

by your insurance company. Your insurance company will

send an insurance 1055 adjuster to assess the damage to

your vehicle before authorising the repairs.

back to top

5.1 Betterment

It is applied when in the course of repairing an accident-

damaged vehicle (age of vehicle is five years and above),

an old part is replaced with a new franchise part. You will

have to bear the difference in cost (depending on the

age of your vehicle) as your repaired vehicle is in a better

condition than it was before the accident.

back to top

5.2 Compensation for Assessed Repair Time (CART)

- CART means a reasonable amount payable by third

party insurance companies as compensation for 1055

of use of vehicle.

- You can only claim for CART if you are not the party

at fault in the accident.

- The number of days allowed for CART is based on

insurance 1055 adjuster's recommendation on the

number of working days estimated to repair the

accident-damaged vehicle and not the number of

days the accident-damaged vehicle is at the workshop.

- Where receipts are produced for vehicle rentals (only

from a licensed car rental company), insurance

companies shall pay the amount shown on the receipt

and original car rental agreement, subject to the condition

that the vehicle rented is of an equivalent model to that

of the damaged vehicle. The number of days allowed is

based on the insurance 1055 adjuster's recommendation

on the number of working days estimated to repair the

accident-damaged vehicle.

back to top

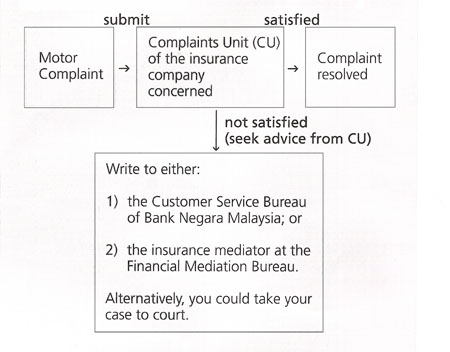

6.0

How to lodge a complaint and redress avenues available?

back

to top

|